Precision Fermentation

10

%

5.5

The only AI-powered strategic intelligence platform that transforms global market shifts into high-impact decisions for food & beverage leaders navigating industry disruption.

Precision fermentation is poised to revolutionize the food and beverage industry by offering more sustainable and efficient methods for protein production. This technology can lead to significant reductions in environmental impact and resource usage, vital for long-term food security.

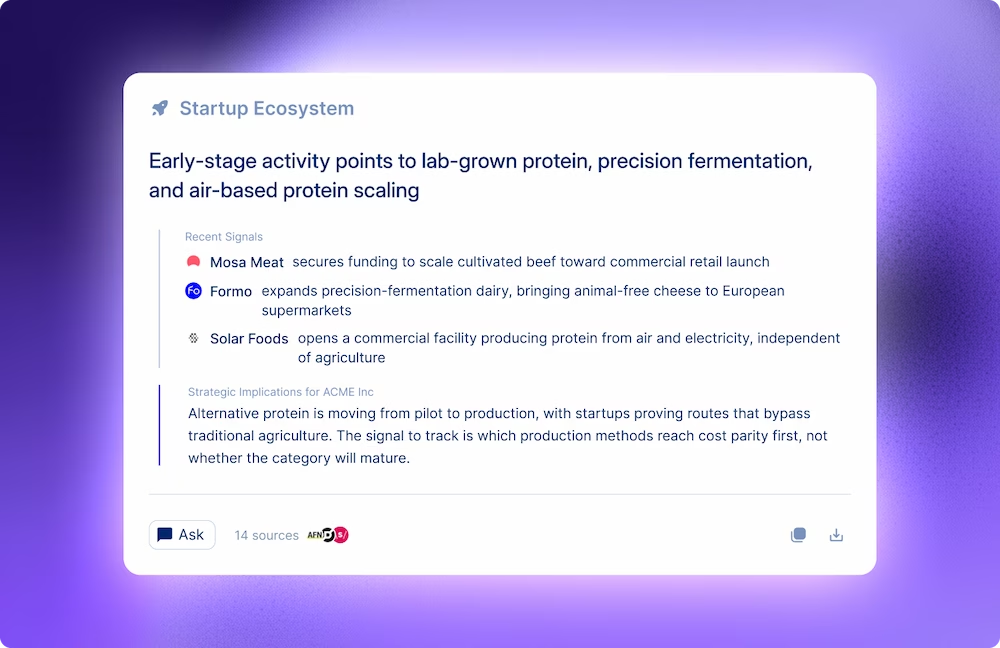

Precision fermentation reduces the reliance on traditional animal-based ingredients, leading to cost reductions and increased control over ingredient quality. Consumer demand shifts towards sustainable and plant-based products, impacting competitor strategies and enhancing brand loyalty for companies embracing this technology. Investments in fermentation technologies boost operational efficiency and innovation in product formulations, particularly in creating alternative proteins and ingredients. Companies aligning with precision fermentation witness increased investor interest due to the scalability and sustainability of the technology

Invest in scaling precision fermentation technologies to enhance product innovation, decrease dependency on traditional agriculture, and meet consumer demand for sustainable and high-quality protein alternatives. Consider partnerships with tech firms for improved process efficiency, aligning with trends in health, sustainability, and technological advancement.

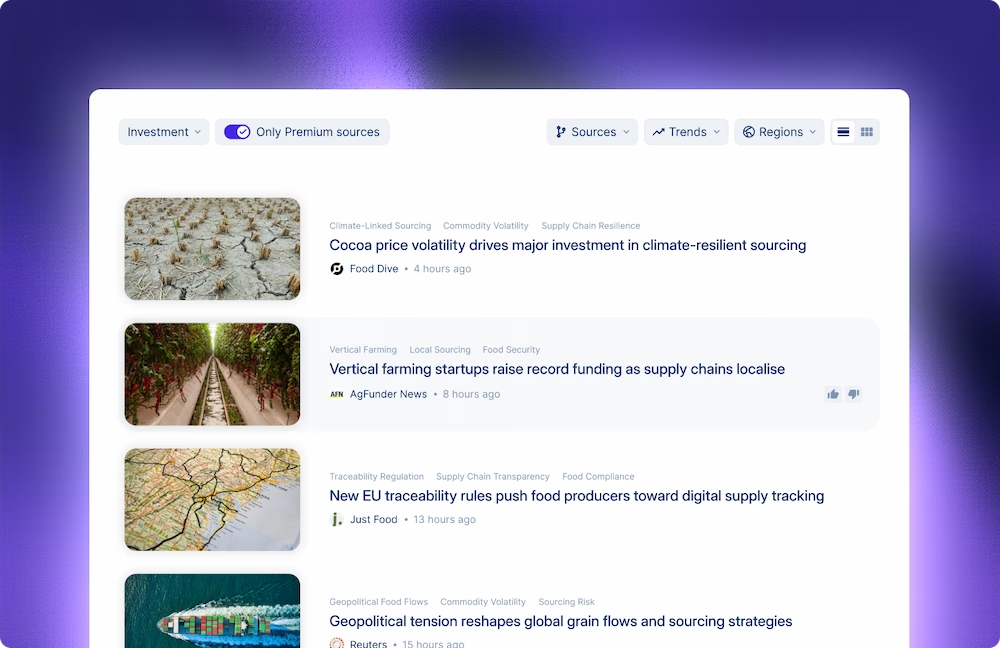

Supply chain transparency is increasingly vital, driven by rising consumer demand for verified product origins and ethical sourcing practices. Technologies like blockchain and AI enhance traceability, supporting regulatory compliance, consumer trust, and competitive advantage for food and beverage companies.

Companies adopting AI and advanced technologies streamline operations, reduce costs, and maximize production efficiency. Improved inventory management and enhanced traceability lead to better compliance, sustainability, and resource allocation. Advanced AI tools impact suppliers by increasing expectations for efficient traceability and quality raw materials. Increased consumer trust follows from reliable and transparent sourcing. Regulatory frameworks may evolve as traceability practices become essential across the industry.

To enhance supply chain transparency, the company could invest in blockchain technology, simplifying traceability for ingredients and driving trust with consumers. This will align with rising consumer expectations for sustainable sourcing and regulatory compliance, benefiting product safety and customer loyalty. However, implementation may require overcoming initial cost barriers and technical challenges.

The acquisition of Huel by Danone highlights the growing focus on functional nutrition, particularly "complete nutrition" products, emphasizing the trend towards health-focused diets and consumer demand for convenience paired with nutritional benefits.

Functional nutrition trend directly impacts product portfolios, prompting acquisitions like Danone's Huel to enhance their health-focused offerings and tap into consumer demand for complete, nutritionally balanced solutions. Increased focus on functional nutrition drives innovation in meal solutions and beverages, requiring companies to adapt sourcing strategies and optimize ingredient quality to cater to rising health-conscious consumer demands.

Invest in research and development of functional drinks that support mood and mental well-being, reflecting growing consumer interest in brain health. This approach could align with social trends focusing on mental health and wellness, ultimately contributing to enhanced customer engagement.

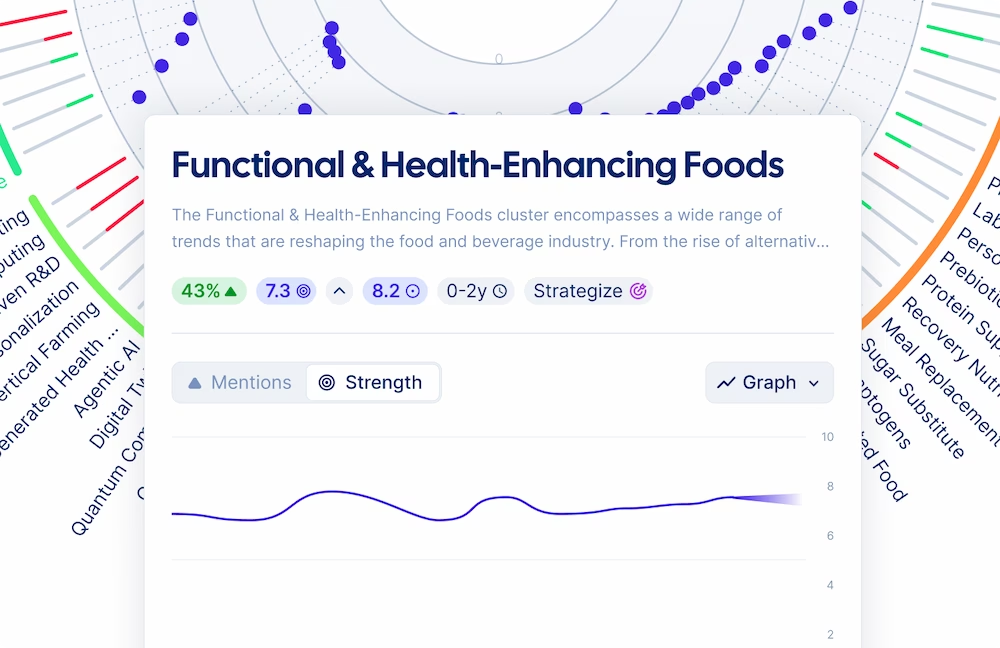

Trendtracker uses a three-layer framework - domains, macro trends, and granular micro-trends - that can be configured to any level of specificity. Leading F&B companies don't set up the platform at the broad "food and beverage" level; they track hundreds of sub-category trends including specific product formats, ingredient directions, and technology signals.

Yes. Trendtracker tracks early-stage signals from the moment mentions begin to climb across {{sources}} vetted news, patent, academic, and market sources, forecasting whether each trend is likely to grow or stay marginal, so teams can move on the ones with staying power. Because the platform draws from vetted sources rather than social-media engagement data, it works best as a complement to social listening, not a replacement for it.

Yes - this is a core use case for large F&B companies where different teams have fundamentally different needs. Each team can build its own trend board with a distinct context: an open innovation team can configure a board focused exclusively on technology signals (patents, academic research, startup activity), while a consumer insights team tracks behavioral shifts, occasion-based trends, and cultural movements.

It depends on where strategic foresight sits in the organization. In consumer goods companies, Trendtracker most commonly enters through an insights, open innovation, or corporate strategy team. From there, it tends to expand to adjacent teams over time as the trend infrastructure gets established. Each team gets its own relevant lens on the same underlying intelligence.

Trendtracker continuously monitors {{sources}} curated sources, automatically scores trends, and generates strategic summaries without manual input - so teams spend their time on interpretation and strategic decisions rather than data collection. The intelligence never stops updating, even when the team is focused elsewhere.